|

|

- 국제법률연구원(ILRI)은

2001년부터 국가별 현지

로펌들과 해외법인설립

온라인 시스템인 "오이오스

(OIOS: Overseas Incorporation

On-line System)"를

개발하여

서비스를 제공하고 있으며

설립후

이사회/주주총회/세금/연례보고 등

법인운영을

대행하는

BIK

서비스도

제공하고

있습니다.

- (참고.

http://www.ilri.co.kr/law4.htm

미국의

경우 www.sos.주이니셜(ca/ms

등).gov 에서 설립안내)

|

- Establish

a company

in your

desired

country,

Business

setup

in around

world.

International

Legal

Research

Institute(ILRI)

is committed

to its

promise

of empowering

clients

and

investors

by offering

a cost-effective

and

world-class

economic

zone

with

customisable

packages

and

services.

We connects

investors

to growing

markets.

Select

your

suitable

legal

entity,

license

type

and

facility.

We'll

guide

you

from

filling

out

your

application

all

throughout

submission,

ensuring

that

all

requirements

are

met.

Your

license

will

be issued

along

with

your

registration

and

bank

account

will

be opened

upon

completion

of the

registration,

then

proceed

the

visa

application

process.

Business

setup

in around

world!

-

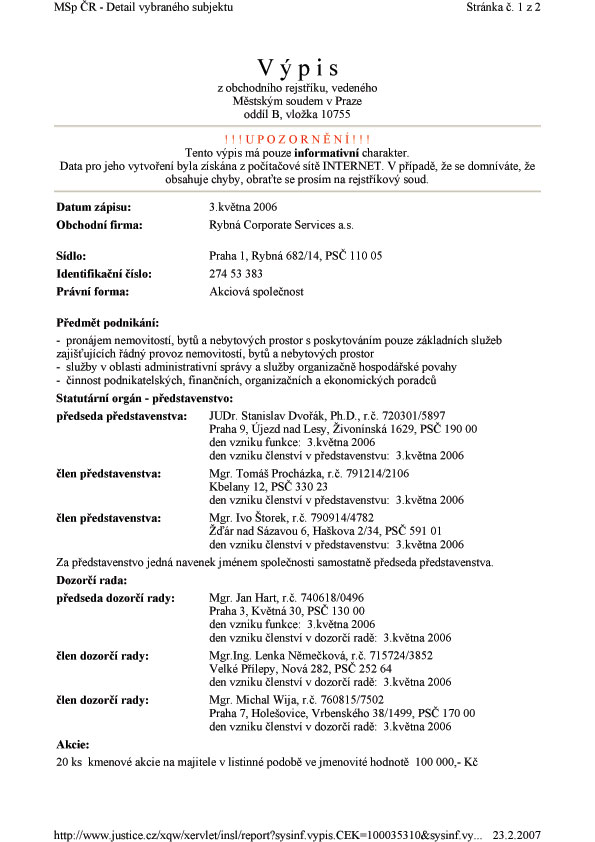

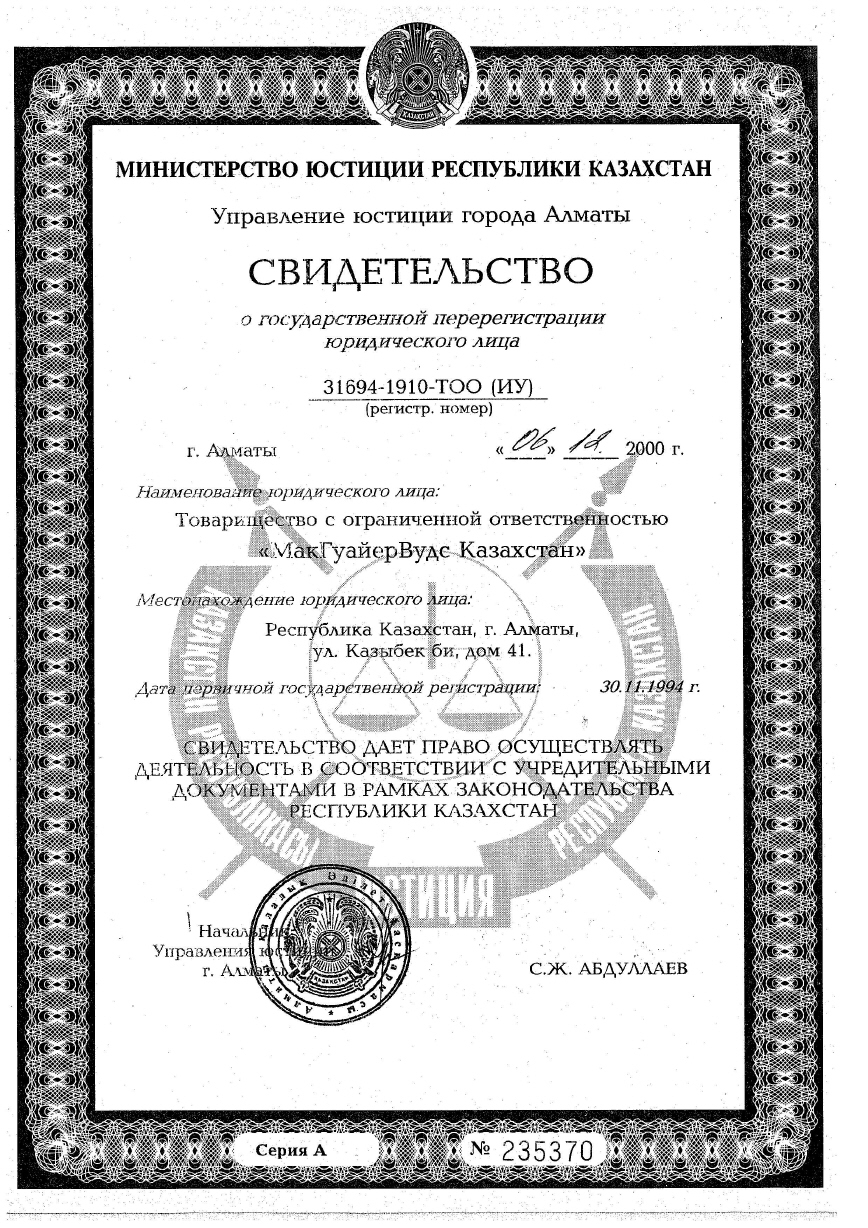

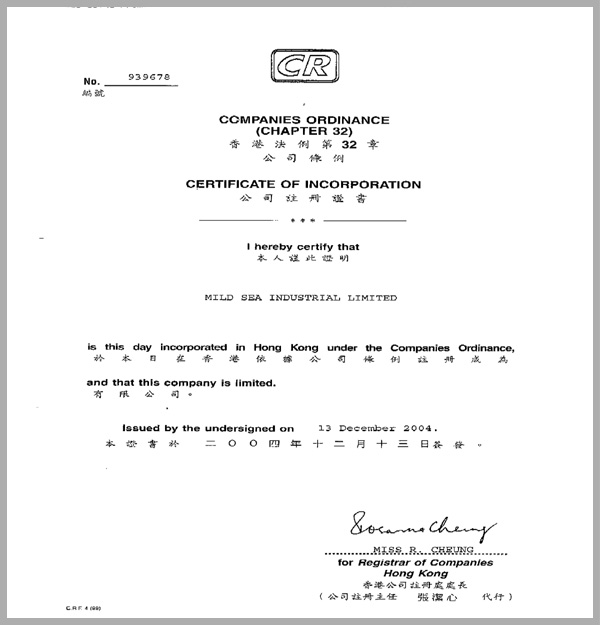

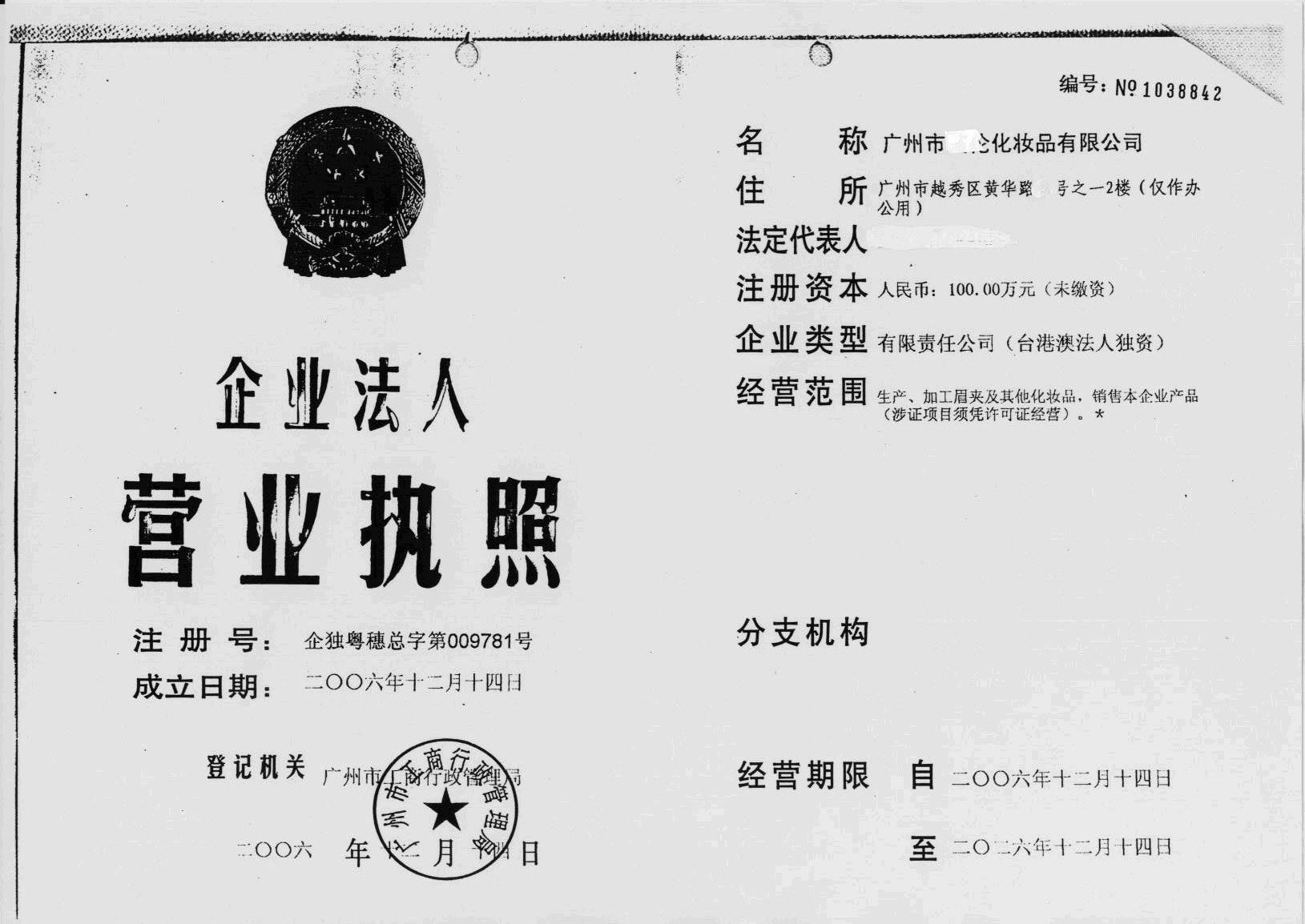

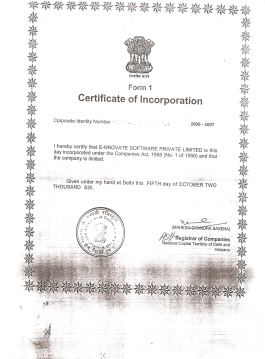

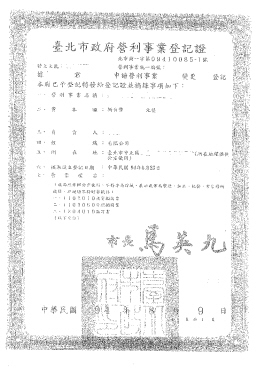

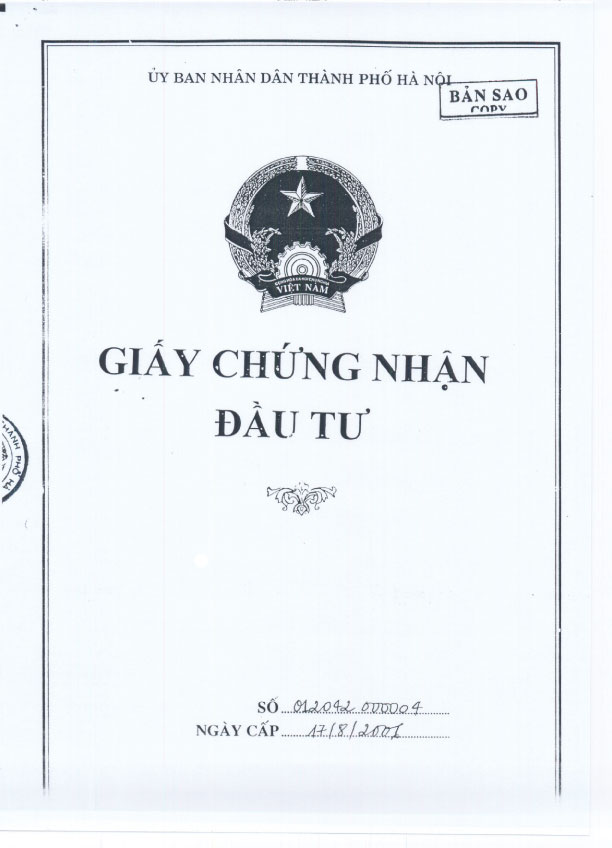

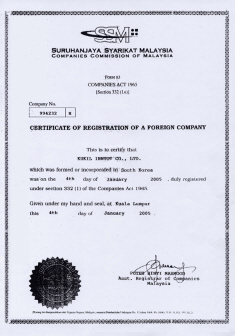

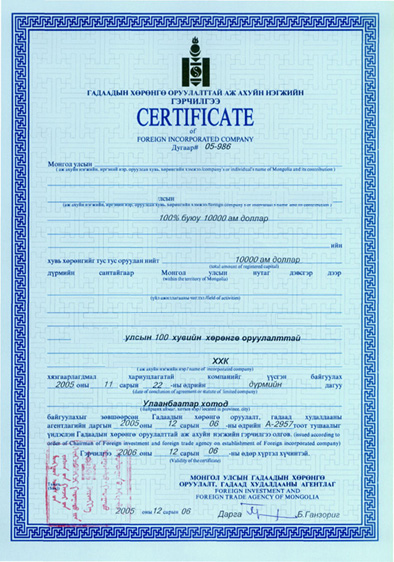

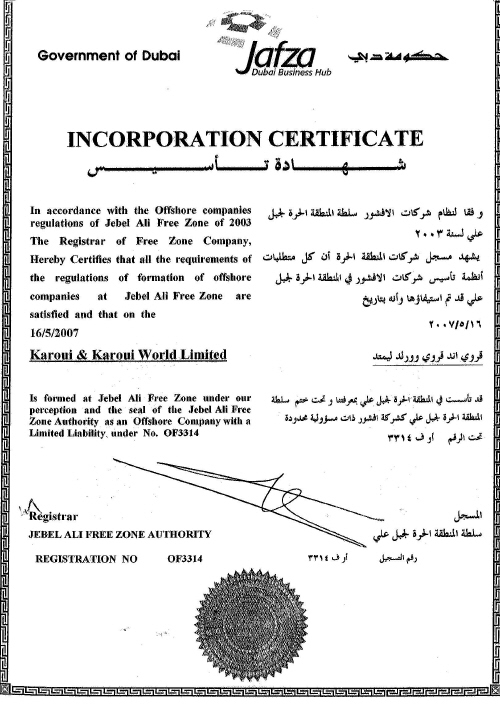

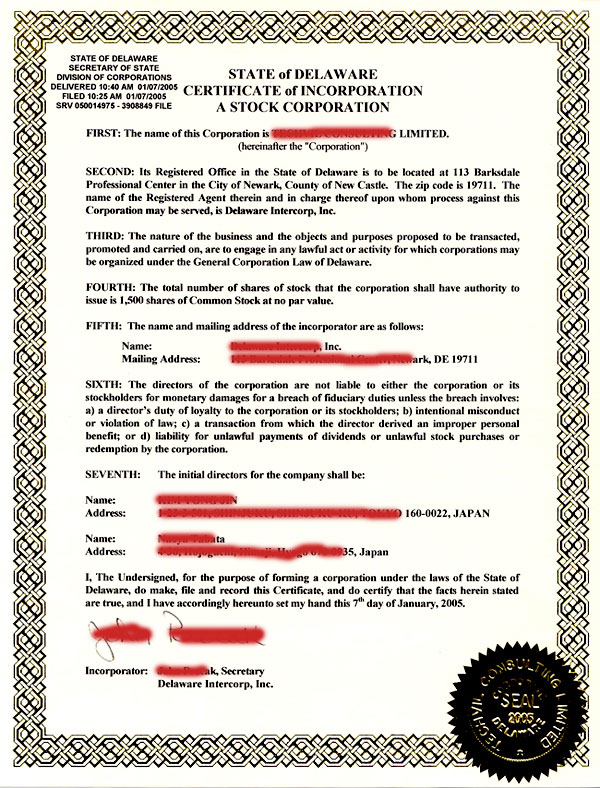

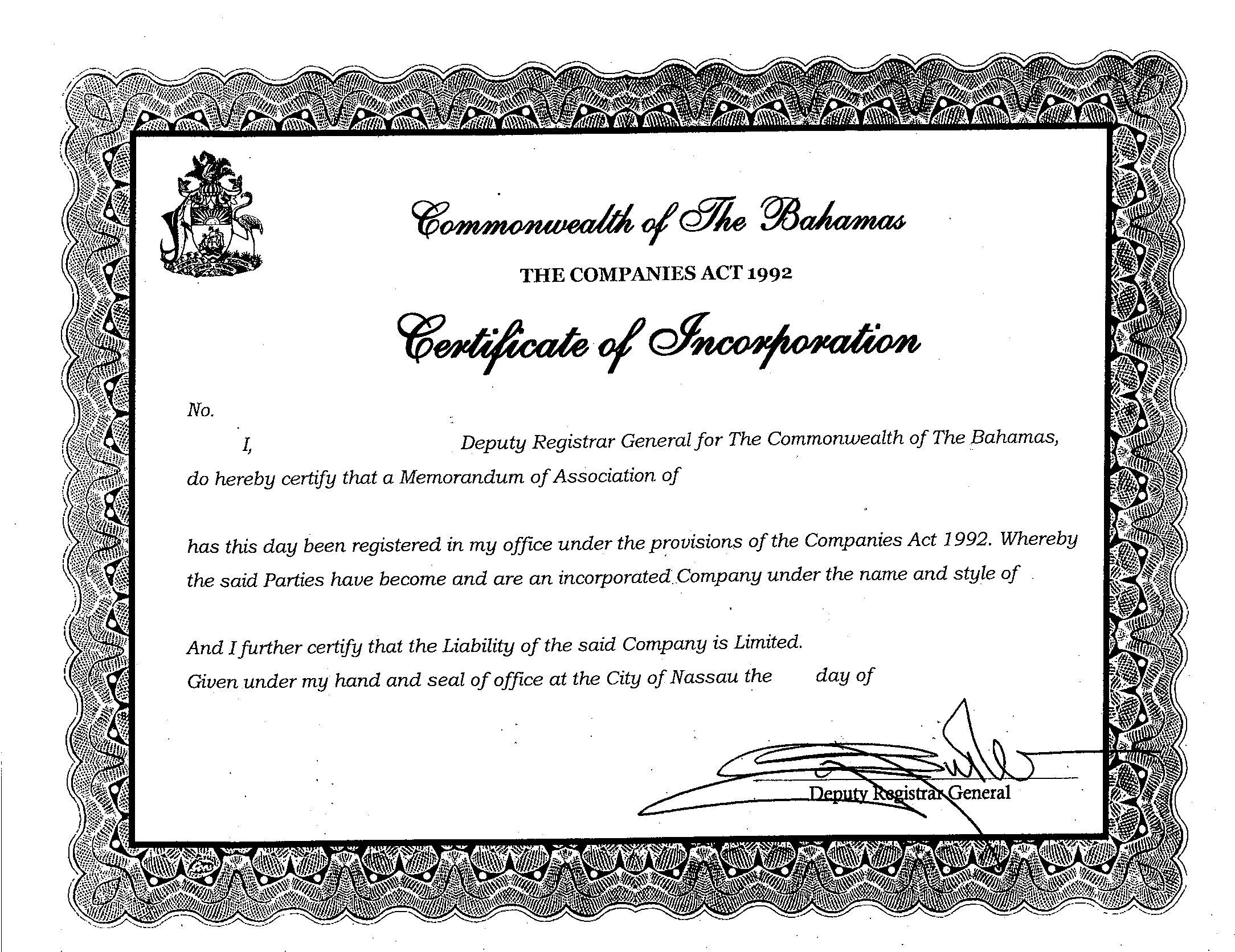

- 해외법인

등기증 국제법률연구원 동의없이 이미지 사용금지.

|

- 미주

(North-South

America)

|

미국(USA)

미국(USA)

|

캐나다(CANADA)

캐나다(CANADA)

|

바하마(BAHAMA)

바하마(BAHAMA)

|

|

|

|

버뮤다(BERMUDA)

버뮤다(BERMUDA)

|

칠레(CHILE)

칠레(CHILE)

|

코스타리카(COSTA RICA)

코스타리카(COSTA RICA)

|

|

|

|

브라질(BRAZIL) 브라질(BRAZIL)

|

멕시코(MEXICO)

멕시코(MEXICO)

|

아르헨티나(ARGENTINA) 아르헨티나(ARGENTINA)

|

|

|

|

베네주엘라(VENEZUELA)

베네주엘라(VENEZUELA)

|

파라과이(PARAGUAY)

파라과이(PARAGUAY)

|

도미니카공화국(DOMINICAN

REPUBLIC)

도미니카공화국(DOMINICAN

REPUBLIC)

|

|

|

|

- 콜롬비아(COLOMBIA)

|

-

|

-

|

|

-

|

-

|

- 유

럽

(EUROPE)

|

프랑스(FRANCE)

프랑스(FRANCE)

|

독일(GERMANY)

독일(GERMANY)

|

영국(United

Kingdom) 영국(United

Kingdom)

|

|

|

|

이탈리아(ITALY) 이탈리아(ITALY)

|

네덜란드(NETHERLANDS)

네덜란드(NETHERLANDS)

|

노르웨이(NORWAY)

노르웨이(NORWAY)

|

|

|

|

스위스(SWISS)

스위스(SWISS)

|

벨기에(BELGIUM)

벨기에(BELGIUM)

|

아일랜드(IRELAND)

아일랜드(IRELAND)

|

|

|

|

핀란드(FINLAND)

핀란드(FINLAND)

|

덴마크(DENMARK)

덴마크(DENMARK)

|

스페인(SPAIN) 스페인(SPAIN)

|

|

|

|

오스트리아(AUSTRIA)

오스트리아(AUSTRIA)

|

체코(CZECH REPUBLIC)

체코(CZECH REPUBLIC)

|

헝가리(HUNGARI)

헝가리(HUNGARI)

|

|

|

|

스웨덴(SWEDEN)

스웨덴(SWEDEN)

|

러시아(RUSSIA)

러시아(RUSSIA)

|

카자흐스탄(KAZAKHSTAN)

카자흐스탄(KAZAKHSTAN)

|

|

|

|

슬로바키아(SLOVAKIA)

슬로바키아(SLOVAKIA)

|

-

슬로바키아(SLOVAKIA)

|

-

슬로바키아(SLOVAKIA)

|

|

|

|

폴란드(POLAND)

폴란드(POLAND)

|

우크라이나(UKRAINE)

우크라이나(UKRAINE)

|

-

|

|

|

-

|

- 오세아니아(OCEANIA) &

아시아(ASIA)

|

뉴질랜드(NEW ZEALAND)

뉴질랜드(NEW ZEALAND)

|

호주(AUSTRALIA)

호주(AUSTRALIA)

|

피지(FIJI)

피지(FIJI)

|

|

|

|

홍콩(HONG KONG)

홍콩(HONG KONG)

|

중국(CHINA)

중국(CHINA)

|

인도(INDIA)

인도(INDIA)

|

|

|

|

마카오(MACAO)

마카오(MACAO)

|

대만(TAIWAN)

대만(TAIWAN)

|

베트남(VIETNAM)

베트남(VIETNAM)

|

|

|

|

태국(THAILAND)

태국(THAILAND)

|

-

태국(THAILAND)

|

필리핀(PHILIPPINE)

필리핀(PHILIPPINE)

|

|

|

|

말레이시아(MALAYSIA)

말레이시아(MALAYSIA)

|

인도네시아(INDONESIA)

인도네시아(INDONESIA)

|

싱가폴(SINGAPORE)

싱가폴(SINGAPORE)

|

|

|

|

일본(JAPAN)

일본(JAPAN)

|

몽골(MONGOLIA)

몽골(MONGOLIA)

|

파키스탄(PAKISTAN)

파키스탄(PAKISTAN)

|

|

|

|

- 아랍

에메레이트

연방(UAE)

|

- 두바이

|

- 사우디아라비아(SAUDI

ARABIA)

|

- 아부다비(ABU

DHABI)

|

|

- 1. To reserve the proposed

company name at Ministry of Commence 2일.

2. To submit investment application to

Saudi investment Authority(SAGIA) and obtain SAGIA License 15일.

3. To submit the Article of Association

of the Company to Ministry of Commerce for study to be approved.

4. To notarize the Articles of

Association of the company before the Notary Public 3주.

5. To publish a brief of the Article of

Association of the Company in the Gazette (Umm Alqura news paper) 2일.

6. To submit application to the Ministry

of Commerce to obtain the commercial registration (CR) 3주(and this stage requires appointing the Company Manager and enter to

Saudi Arabia and obtain the work permit and residence permit (Iqama) depositing

the company

capital in recognized Saudi Bank, lease contract for the company location and

register the company at Chamber of Commerce.)

7. Open company files In General

Insurance Organization (GOSI) and Zakat and Income Tax Department 4일.

8. Obtain the Investment License. Total

time of finalizing the procedures up to obtain the company CR 45일.

- ㅁ 비용:

- - 국내: 5백만원

- - 국외: 5만SAR Professonal fee + Government

fee(Sagia License SAR2.000, Statues

publishing SAR500, Commercial Register/1 year SAR1.200, Chamber of

Commerce/1year SAR2.100, File Submitting SAR1.000, Diverse incidentals SAR750, Name

publishing(if required) SAR900.)

- ㅁ 제공:

- - issuing a true copy of SAGIA

license

- - drafting, AOA

- - incorporating & notarizing

the AOA

- - issuing CR and CCI

subscription.

- - Open company files In General

Insurance Organization (GOSI) and Zakat and Income Tax Department.

- - Providing the complete list of

the required documents.

- - Reserving & publishing the

“Trade Name” of the Company, if needed.

- - Preparing & submitting the

“Investment File” to the concerned authority “Sagia”, and following the process

until license issuing.

- - Preparing & submitting the

company's Articles of Association to the Ministry of Commerce, and following

the process to get the final approval.

- - Legalizing the AOA by a notary

public & publishing them in a newspaper.

- - Preparing & submitting the

necessary applications [the required documents File] and maintaining a

permanent follow up with respect to the issuance of the Commercial Registration

Certificate and the Chamber of Commerce participation, provided that you

achieve within the predetermined time, the deposit of the capital of the

company in a Saudi Bank.

- - Submitting an application for

the Company Recruitment Number.

- * SAGIA: Saudi Arabia foreign

Investment Authority.

- * AOA: Article of Association.

- * CR: Commercial Registration.

- * CCI: Chamber of Commerce and

Industry.

- ㅁ 구비서류:

- 1. Shareholders resolution to invest in Kingdom of

Saudi Arabia stating the shareholders names, capital, shares percentage (stock

or cash) location, activities and appointing the General Manager notarized and

authenticated from the 주한 Saudi 대사관.

2. Copy of the Commercial Registration

for each participating company

authenticated from the 주한 Saudi embassy translated to

Arabic language and from 국제법률연구원 같은 recognized

translation office.

3. Copy of Articles of Associations of

each company, authenticated from

the competent authority and the 주한 Saudi embassy,

translated to Arabic language from 국제법률연구원 같은recognized

translation office.

4. Passport copy for all partners and

the appointed General Manager

(all papers) accompanied with 4 original personnel photos (in white background)

for each.

5. Non objection letter from the last

sponsor if the General Manager have been reside in Saudi Arabia within last

three years.

6. Copy of last two years budget for the

company prepared by and authenticated from auditing office in the investor's

country and approved from the related official commerce or taxes office to be

authenticated from the 주한 Saudi embassy. translated to

Arabic language from 국제법률연구원 같은 recognized translation

office.

7. The principal Articles of Association

of the new company complying with the Saudi ministry of commerce and industry

laws (we shall draft it)

8. Power of attorney for our law firm to

proceed establishing the

company on behalf authenticated from the 주한 Saudi

Embassy. (we

shall provide the draft of it).

- The requirements of contracting

activity (in addition to the above stated general required documents) are as

follow:

1- Provide the budget for the company

owned by a foreign investor outside the Kingdom for three years prior to

application for a license show the integrity of the financial situation of it

prepared from accredited accountant office and authenticated from the tax

authority on the country of the investor and Saudi Embassy.

2- Presence of a distinguished works

done by the company previously in the field of activity which would like to

invest in accompanied with the obtained certificates of achievement.

3- The company should be classified in

its country with the same activity, and not less rating for the third degree or

equivalent authenticated from the Saudi Embassy.

4- provide bank certificate stating that

each partner share is not less than(SR. 250.000) authenticated by the Saudi

Embassy.

5- The legal entity should be a limited

liability company.

6- To provide a timetable for the steps

to implement the project.

7- To provide Acknowledgment committing

to deposit the company capital in a licensed Saudi bank after the issuance of

investment license and certificate of deposit in the name of the company before

obtaining the commercial registration (We shall do the required Arabic

translation for above documents by recognized translation office in KSA)

ㅁ 조세제도: Any foreign partner will be 20% of his (or

its) net annual profit, in addition to 5 % on the profit dividends. It is

important to know that any Saudi partner will only pay 2, 5% (Zakat) on his

part.

|

-

|

|

-

|

|

-

|

- 아프리카(AFRICA)

|

-

|

-

|

- 카메룬(CAMEROON)

&

OAPI

|

탄자니아(TANZANIA)

탄자니아(TANZANIA)

|

|

|

|

|

|

|

|

|

|

-

해외법인

형태별

장단점 (국제법률연구원

www.ilri.co.kr

자료 무단사용 엄금) 해외법인

형태별

장단점 (국제법률연구원

www.ilri.co.kr

자료 무단사용 엄금)

|

- 회사종류

|

- Annual

- Meeting

|

- 주식거래

|

- 장점

|

- 단점

|

- 1.

Sole Proprietorship

|

- 비의무

|

- 주식없음

|

- • 설립 간편

- • 결정권이

오너에게 있어 결정이 신속. 수익은 오너의

몫

- • 법적 구속이

적음

- • 폐업

간편

- • 낮은

세금

|

- • 직원채용

어려움

- • 자금 조달

어려움

- • 외부자본

유입불

- • 존속기간이

한정적

- • 사업주

무한책임

|

- 2. General

- Partnership

|

- 비의무

|

- 자유

|

- • 2인 이상이

결합한 것외에는 개인회사와 비슷

- • 조합은 개인간, 회사간, 신탁간, 다른

파트너간 연계 가능

- • 설립 간단

- • 조직과 의사결정 과정 유연.

- • 파트너의

능력과 기량 충분 발휘

- • 자금조달

용이

- • 파트너들이 사업에 적극적

- • 법적입장명확

- • 수익에 대한

직접 과세가 없고, 자본 배분에 의한 이익, 손익을 개인소득 수준으로 과세.

|

- • 회사부채에

파트너들의 무한책임

- • 파트너십에

대한 청구에 개인책임을 보호받지 못함

- • 파트너십

존속기간만 사업 진행

- • 파트너 사망시 사업 종료.

- • 결정권이 분산되어 있어 파트너들간의 동의로 구성

- •

구두상 동의 가능하지만 문서동의가

의견 대립 해소

예방.

|

- 3. LP

- (Limited Partnership)

- (합자회사)

|

- 비의무

|

- 자유

|

- • 1인 이상의

무한책임출자자와 유한책임출자자가 각 1인 이상으로 결합한 2인

이상의 파트너십 회사.

- • 무한책임출자자는 회사채무에 대한 무한책임

- • 유한책임출자자는 약속한 자산 범위내에서만

책임

|

- • 유한출자자는 경영 권한이 없음

|

- 4. LLP

- (Limited Liability Partnership)

|

- 비의무

|

- 자유

|

- • 모든 파트너들

유한책임 보호받음

|

- • 현재 파트너십이

Corporation

Bareau에

양식

DSCB:15-820A로

신고해야 함

|

- 5.

C corporation

- (주식회사)

|

- 의무

|

- 자유

|

- • "C"는

사업구조형태가 아닌 세금지위상태를 의미

- • 주주 유한책임

- • 회사 영구존속

- • 임원 변경

간단

- • 사업 확장 간단

|

- • 세금은 회사와

주식배당금을 맏은 주주들이 납부

- • 회사의 손실

공제 받을 수 없음

- • 법적 구속이

많음

- • 경비 내용의

계약을 체결해야함

- • 법인과 주주에게

이중으로 과세함

|

- 6.

S corporation

|

- 의무

|

- 자유

|

- • "S"는

사업구조

형태가 아닌 세금지위상태를 의미

- • 장점은 보통

법인과 동일

- • 법인 수준의

과세는 없으며, 파트너십과 유사한 세제 혜택

|

- • 주주 수

제한(최대 75명)

- • 투자를 유치할

수있는 %에 제한

- • 연방에서

S 지위를 얻지 못하면

S Corporation

불가

- • Capital Stock Tax 납부의무는 다른 회사들과 같음

- • 다른 법인

또는 비거주자 외국인은 주주가 될 수 없음

- • 자회사를

소유할 수 없음

|

- 7. LLC

- (Limited Liability Company)

|

- 비의무

|

- 승인필요

|

- • 주식회사와

파트너십의 혼합 형태

- • 주식회사의

유한책임의 유리한 점과 파트너십의 유리한 점을 결합

- • 구성원은

법인과 같이 유한책임

- • 법인 수준의

과세는 없으며 구성원 개인에게 과세됨

- • 구성원 수의

제한이 없음

|

- • 존속기간

한정적

- • 사업형태로

인정된 역사가 짧아 법률의 적용 및 해석이 주에 따라 불일치

|

- 8.

Joint Stock

|

-

|

-

|

- •

외국투자자

현지투자자 공동출자

|

- •

출자비율에

따라 권리/손익 분배.

|

- 9.

Joint Venture

|

-

|

-

|

- •외국투자자

현지투자자 공동출자

|

- •

계약에

따라 권리/손익 분배.

|

|

- 회사

종류별

특징

|

-

- 목차

-

- 1.

Corporation 개요

- 2.

S corporation,

C

Corporation

특징

- 3.

Limited liability company(LLC)

특징

-

4.

Professional Entity.

PC, PLLC 특징

-

|

- 1.

Corporation 개요

|

- 코퍼레이션은

소유주와

별개로

설립

가능.

- A corporation is a legal entity that can

exist separately from its owners.

- Creation of a corporation occurs when properly

completed articles of incorporation (called a charter or certificate of

incorporation in some states) are filed with the proper state authority, and all

fees are paid.

-

- 서류작성.

- What paperwork is required to

incorporate?

Articles of incorporation conforming to state law must be

prepared and filed with the proper state authorities and filing fees, initial

franchise taxes, and other initial fees must be paid. If you incorporate

through Business Filings Incorporated, all you need to do is complete the online

order form, and Business Filings prepares and files your articles of

incorporation. Additionally, the price you pay includes all filing fees.

-

- 회사명

선택.

- What should I name my

corporation?

- Choose the name of your corporation carefully. It is very

important that you portray the image you want for your new corporation. Legally,

the name you select must not be "deceptively similar" to any existing

corporation or must be "distinguishable on the record" of your state. For

example, if a corporation named Flower Corp. exists in your state, you probably

would not be allowed to name your business Flour, Inc. It is possible that the

name you select will not be available; therefore, we ask for a second choice on

the incorporation order form. Additionally, the name you choose must show

your business is incorporated. Most states require that the corporate name be

followed by some type of indicator, such as Corporation, Incorporated, or an

abbreviation.

-

- 장점.

- What are the advantages of incorporation?

- One of

the primary advantages of incorporation is the limited liability the corporate

entity affords its shareholders. Typically, shareholders and directors are not

liable for the debts and obligations of the corporation; thus, creditors will

not come knocking at the door of a shareholder or director to pay debts of the

corporation. In a partnership or sole proprietorship the owner's personal assets

may be used to pay debts of the business. Maintaining the limited liability of a

corporation requires that the shareholders and directors follow all the rules of

governance, including holding annual meetings and maintaining meeting minutes,

which is why we offer corporate forms disks and corporate kits as part of our

complete incorporation package.

Other advantages:

- A corporation's

life is not dependent upon its members. A corporation possesses the feature of

unlimited life. If an owner dies or wishes to sell his or her interest, the

corporation will continue to exist and do business.

- Retirement

funds and qualified retirement plans (like 401k) may be set up more easily with

a corporation.

- Ownership of a corporation is easily transferable.

- Capital can be raised more easily through the sale of stock.

- A corporation possesses centralized management.

-

- 단점

- What are

the disadvantages of incorporation?

- The primary disadvantage to a corporation

is double taxation. Profits of a corporation are taxed twice when the profits

are distributed to shareholders as dividends. They are taxed first as income to

the corporation, then as income to the shareholder. All reasonable business

expenses such as salaries are deductions against corporate income and can

minimize the double tax. Further, the double tax can be eliminated by making an

S corporation election.

Other disadvantages:

- There is more

complexity and expense with forming a corporation.

- There are more

extensive record keeping requirements.

- Operating a corporation

across state lines often requires the corporation to qualify to do business in

the other state.

-

|

- 2.

S corporation

및

C

Corporation

|

-

- 세금

- Standard business

corporations or C corporations are required to pay income tax on taxable income

generated by the corporation. Making a subchapter S election by completing and

filing federal Form 2553 with the IRS is a way to avoid having your corporation

treated as a separately taxable entity. An S corporation is a standard

business corporation that has elected a special tax status with the IRS. This

tax treatment allows the corporation not to be a separately taxable entity.

Instead, the income of the corporation is treated like the income of a

partnership or sole proprietorship; the income is "passed-through" to the

shareholders. Thus, shareholder's individual tax returns report the income or

loss generated by an S corporation. To be classified as an S corporation, a

corporation must make a timely filing of Form 2553 to the IRS. This election

must be made by March 15 if the corporation is a calendar year taxpayer, in

order for the election to take effect for the current tax year. A corporation

may later decide to elect S corporation status, but this decision would not take

effect until the following year. In order to qualify for S corporation

status, the S corporation can have no more than 75 shareholders and must make

the election to be an S corporation. The shareholders cannot be non-resident

aliens. Also, an S corporation cannot issue preferred shares of stock with

special liquidation, dividend, or conversion rights. To compare the S

corporation to the C corporation and limited liability company, view our

comparison page.

-

- 회사구성

- What is the organizational structure of a

corporation?

- The organizational structure of a corporation relies on three

basic groups: shareholders, directors, and officers. A corporation is owned

by shareholders; however, they do not directly manage the corporation. Instead,

they influence corporate decisions through indirect methods such as electing and

removing directors, approving or disapproving amendments to the articles of

incorporation and voting on major corporate issues. The directors, who

comprise the "board of directors," are responsible for managing the affairs of

the corporation. Usually, directors make only the major business decisions and

supervise and appoint the officers who make the day-to-day business decisions of

the corporation. Officers are responsible for the everyday management of the

corporation. Typically, officers are appointed directly by the board of

directors. It is important to note that a shareholder may serve on the board

of directors and as an officer. In fact, in most states one person is enough to

form a corporation.

-

- 설립

이사의

수

- How many directors do I need to form a

corporation?

- Only one director is required in most states although you can

elect to have more. Some states use the number of shareholders in the

corporation to determine the minimum number of directors. If the number of

shareholders is three or more, then the corporation must have three directors.

If the corporation has less than three shareholders, then the number of

directors may equal the number of shareholders.

-

- 회사등록처

- Where should I

incorporate my business?

- One of the first decisions a business must make

after deciding to incorporate involves selecting the proper state of

incorporation. A corporation is not required to incorporate in the state of its

operations; however, often the best decision may be to incorporate in your home

state.

Two issues must be weighed to determine the proper state: (1) a

dollars and cents analysis comparing the costs of incorporating in the state of

operation versus qualifying to do business as a foreign corporation in the state

under consideration and (2) determining the advantages and disadvantages of each

state's corporate laws and tax structure. If the corporation is a closely

held corporation and does business primarily within a single state, local

incorporation is often preferable. The cost of local incorporation will usually

be less than incorporating in another state and qualifying to do business as a

foreign corporation in the state. A foreign corporation that qualifies to do

business in another state is subject to taxes and annual report fees from both

the state of incorporation and the qualifying state. Another disadvantage of

incorporating outside of your home state is the possibility of having to defend

a law suit in another state. For advice regarding which state is optimal for

your particular business situation, consult an attorney or an

accountant. During the life of your business, if you find that your company

needs to foreign qualify to transact business in another state, Business Filings

can assist with this process.

-

- 설립공고

- What is a publication

requirement?

- A few states require notice to be published in a newspaper that

a corporation or LLC has been formed. States with this requirement include:

Pennsylvania (corps only), Georgia (corps only), Arizona (corps and LLCs),

Nebraska (corps and LLCs), and New York (LLCs only). The filing performed by

Business Filings completes the publication requirement for each of the states

except for New York LLCs.

-

- 설립절차

- How do I get started with the

incorporation process?

- If you choose to incorporate, articles of

incorporation must be filed with that state and initial fees must be paid.

Business Filings will complete these administrative tasks quickly and

effectively. After your articles are filed, your corporation must hold an

organizational meeting where bylaws are adopted and the incorporation process is

completed. Share certificates should be distributed to shareholders and these

transactions should be recorded on the corporation's stock ledger. All of this

information should be kept in a corporate record book. Business Filings'

corporate kit includes all of the information and paperwork needed to make this

process easier.

-

|

- 3,

Limited liability company(LLC)

|

-

- 세금

- How is an LLC taxed?

- A state-registered

LLC can be taxed for federal income tax purposes as a partnership. Under the

check-the-box rules, an LLC can elect partnership status to avoid taxation at

the entity level as an "association taxed as a corporation." If an LLC is not

taxed as a partnership, it will be taxed at the entity level similar to a

standard or C corporation. The state income tax treatment of LLC profits and

losses may or may not mirror the IRS tax treatment depending on the state. For

specific information on your state rules visit your state's web site. The web

address can be found on our detailed state information page. Please note that

California LLCs are subject to an annual minimum franchise tax of $800 per year.

The first payment must be made within 3 months of forming your LLC. The state of

California does send a bill to help you to remember to make this

payment.

-

- 유한책임회사(유한회사)

특징

- The limited liability

company or LLC is not a partnership or a corporation. An LLC is a distinct type

of business that offers an alternative to partnerships and corporations, by

combining the corporate advantages of limited liability with the partnership

advantage of pass-through taxation.

-

- 설립서류

- What paperwork is required to

form an LLC?

- Articles of organization must be prepared and filed with the

state and filing fees, initial franchise taxes, and other initial fees must be

paid. If your LLC is formed through Business Filings Incorporated, all you

need to do is complete our simple order form. We will prepare and file your

articles of organization and pay the initial filing fees.

-

- 설립시

변호사 유무

- Do I

need an attorney to form an LLC?

- No, an attorney is not a legal requirement.

You can prepare and file the articles of organization yourself; however, you

should understand the requirements of your intended state of formation. You

can use our service to form your LLC and save money on attorney's fees. However,

if you are unsure of what entity type would be most beneficial to your business,

consult an attorney or accountant.

-

- 회사명

선택

- What should I name my

LLC?

- Choose the name of your LLC carefully. It is very important that your

name portray the image you want for your new company. Legally, the name you

select must not be "deceptively similar" to any existing company or must be

"distinguishable on the record" of your state. For example, if an LLC named

Flower LLC exists in your state, you probably would not be allowed to name your

business Flour Limited Liability Company. It is possible that the name you

select will not be available; therefore, we ask for a second choice on the LLC

order form. Additionally, most states require that the name you select show

your business is a limited liability company, by including the words "Limited

Liability Company," or the abbreviation LLC.

-

- 구성원수

- How many people are

needed to form an LLC?

- The IRS does allow one member LLCs to qualify for

pass-through tax treatment; however, taxation of one person LLCs at the state

level may be different.

-

- 설립구성

- What is the organizational structure of an LLC?

- An LLC

is owned by its members. They are analogous to partners in a partnership or

shareholders in a corporation, depending on how the LLC is managed. A member

will more closely resemble shareholders if the LLC utilizes a manager or

managers, because then the members will not participate in management. If the

LLC does not utilize managers, then the members will closely resemble partners

because they will have a direct say in the decision making of the company. A

member's ownership of an LLC is represented by their "interests", just as

partners have "interest" in a partnership and shareholders have stock in a

corporation.

-

- 회사운영

- How is an LLC managed?

- An LLC may be managed by

its members (owners) or by selected managers. If the LLC is to be managed by

its members, it operates much like a partnership. Each member has an equal say

in the decision making process of the company. If the members choose, they

may elect a manager or managers to act in a capacity similar to a corporation's

board of directors. These managers are in charge of the affairs of the

corporation. Member management is the normal default rule of state law. This

means that if managers are not selected in the articles of organization, the

members will direct the affairs of the LLC.

-

- 장점

- What are the

advantages of an LLC?

- LLCs offer numerous advantages.

- Pass-Through Taxation:

LLCs allow for pass-through taxation. This means that

earnings of an LLC are taxed only once. The earnings of an LLC are treated like

the earnings from a partnership, sole proprietorships and most S corporations.

- Limited Liability: The LLC owner's liability is generally limited

to the amount of money which the person has invested in the LLC. Thus, LLC

members are offered the same limited liability protection as a corporation's

shareholders.

- Flexible Management Structure and Flexible Ownership

is Permitted: Like general partnerships, LLCs are generally free to establish

any organizational structure agreed on by the members. Thus, profit interests

may be separated from voting interests.

-

- 단점

- What are the

disadvantages of an LLC?

- The disadvantages of an LLC include:

- More Paperwork Than an Ordinary Partnership:

Documents must be filed at the

state level to create an LLC, which is not the case with a general partnership.

- Dissolution Date: Some states require that a dissolution date be

listed in the articles of organization. This date may be amended. Further,

certain events, such as death of a member, a member leaving, bankruptcy, etc.

can be a dissolution event. A corporation has unlimited life and these events

are not dissolution events for a corporation.

- Newer Entity

Type: The LLC is a newer entity, and people are not as familiar with the LLC

as a corporation.

-

- 유한회사와

S

코퍼레이션

선택

- Should I choose an LLC or an S

corporation?

- While the S corporation's special tax status eliminates double

taxation, it lacks the flexibility of an LLC in allocating income to the

owners. An LLC may offer several classes of membership interests while an S

corporation may only have one class of stock. Any number of individuals or

entities may own interests in an LLC. However, ownership interest in an S

corporation is limited to no more than 75 shareholders. Also, S corporations

cannot be owned by C corporations, other S corporations, many trusts, LLCs,

partnerships, or nonresident aliens. Also, LLCs are allowed to have subsidiaries

without restriction. To learn more about the similarities and differences of

S corporations and LLCs, click here. For advice regarding which entity is best

for your particular situation, please contact an attorney or

accountant.

-

- 설립공고

- What is a publication requirement?

- A few states

require notice to be published in a newspaper that a corporation or LLC has been

formed. States with this requirement include: Pennsylvania (corps only), Georgia

(corps only), Arizona (corps and LLCs), Nebraska (corps and LLCs), and New York

(LLCs only). The service performed by Business Filings includes the publication

requirement for each of the above states except for New York LLCs. In New

York, all LLCs formed or foreign qualified there are required to publish a

notice of formation for six consecutive weeks in assigned newspapers. The

publication is made at the county level in two newspapers as assigned by the

local county recorder. The cost of this requirement varies greatly based upon

the county where the business is located. In New York County, the publication

costs will be higher than in the rest of the state. To comply with this

requirement, please contact your local county recorder office and they will

assign the newspapers. The county recorder phone number is located in the blue

pages of your local phone book.

-

- 설립절차

- How do I get started setting up an

LLC?

- After you decide to form an LLC, articles of organization must be filed

with that state and initial fees must be paid. If you choose Business Filings to

form your LLC, we will complete these administrative tasks quickly and

effectively. After your articles of organization are filed, your LLC should

have an organizational meeting where an operating agreement is adopted, interest

certificates are distributed, and other preliminary matters are

completed. Business Filings' LLC kit includes all of the information and

paperwork to make this process easier.

-

|

- 4.

Professional Entity.

PC, PLLC

|

-

- 세금

- How

is a professional entity taxed?

- Generally, the taxation of professional

corporations and PLLCs is the same as standard corporations and

LLCs. Professional corporations are taxed like C corporations (unless

they make the S corporation election). However, some professional corporations

do not have the advantage of graduated corporate federal income tax rates. Those

professional corporations that are "qualified personal service corporations" may

be eligible to pay a flat federal income tax rate of 35 percent. "Qualified

personal service corporations" typically provide services in the fields of

health, law, engineering, architecture, accounting, actuarial science, or

consulting. You should seek the advice of an attorney or accountant regarding

whether your company meets this classification in your state of

formation. Professional corporations are allowed to file for S

corporation status, which allows for the entity to have pass-through tax

treatment. With pass-through taxation, the income to the entity is not taxed at

the entity level; however, the entity does complete a tax return. The income or

loss as shown on this return is "passed through" the business entity to the

individual shareholders or interest holders, and is reported on their individual

tax returns.

-

- PC,

PLLC

회사구분

- What is

a professional corporation or professional limited liability company?

- Professional corporations (PCs) and professional limited liability companies

(PLLCs) are corporations and limited liability companies organized for the

purpose of providing professional services. What services constitute

professional services are defined by state law, and differ from state to state.

Typically, professions that require a license, such as doctors, chiropractors,

lawyers, accountants, architects, or engineers are required to form professional

corporations or PLLCs. Typically, professional corporations or PLLCs must be

organized for the sole purpose of rendering professional services of the

licensed practitioners.

-

- 전문회사

설립

- How

is a professional entity formed?

- The formation documents, the articles of

incorporation for a professional corporation and articles or organization for a

PLLC, are similar to those of standard corporations and LLCs. However, with

professional entities, the proper state licensing body must often approve the

formation documents before these documents can be filed with the secretary of

state. Further, the articles typically must contain the signature of a licensed

professional as the incorporator, and that person's license number typically is

required. Therefore, the filing time for professional entities is longer than

the filing time for standard business entities. Due to the additional

requirements for professional entities, Business Filings Incorporated charges a

fee of $125 in addition to our standard corporation or LLC formation

fees.

-

- 회사명

선택

- What

do I name my professional entity?

- Choose the name carefully. It is very

important that you portray the image you want. The name you select must not be

"deceptively similar" to any existing corporation or must be "distinguishable on

the record" of your state. For example, if a corporation named Smyth Architects

P.C. exists in your state, you probably would not be allowed to name your

business Smith Architectural Design Professional Corporation. It is possible

that the name you select will not be available; therefore, we ask for a second

choice on the incorporation order form. Additionally, the name you choose

usually must show your business is a professional corporation or PLLC. Most

states require that the corporate name be followed by the ending Professional

Corporation or the abbreviations P.C., PC, or in some states P.A. (for

Professional Association). For professional LLCs, the appropriate ending is

Professional Limited Liability Company or PLLC. Depending on your state

of incorporation, there may be restrictions that require the profession to be

listed in the company name (for example, Johnson Chiropractic, PC).

Additionally, there may be specific "restricted words" that are not available

for use in names. Check the state specific page for your intended state of

formation for more

details.

-

- 주주와

임원

자격

- Who

can be a shareholder or director in a professional corporation?

- Many

states restrict who may be a shareholder or a director of a professional

corporation. For example, in some states only licensed practitioners of the

specific service that the corporation provides may own stock in the corporation

and serve on the board of directors. Other states require at least 50% of the

shareholders and directors to be licensed professionals.

|

-

해외법인 혜택 Legal

Benefits of Incorporation

|

-

|

|

|

- 해외연락사무소

Non-profit

Office

|

-

- 공통요건

1.

Active Investement 2. Substantial Investment

3. Marginal Investment

4. Essential Role

-

|

- -

이사, 감사,

자본금 제한

없음

- No

limitation

of Director,

Auditor

as well

as capital.

- -

모기업이

자본금 50%

이상 소유

-

Mother company

owns 50%

of capital.

- -

주거래 은행을

통해 송금(해외직접투자신고수리서,

투자개요서

작성)

- The

capital

or business

expenses

must be

wired by

major correspondent

bank.

|

- -

과거 연간

외화획득실적

미화 1백만불

이상 기업

-

Earning

more than

USD1 million

through

the business

for past

year.

-

- -

주무장관

혹은 회장의

설치 추천을

받은 기업

-

Recommended

by Minister

or KITA

to establish

the business

overseas.

|

- -

비영리 Non-beneficial,

시장조사

Market research,

판로개척

Marketing,

거래상담

Business

consultation,

연구개발

Research

& Development.

- -

설립 자격조건은

지사와 동일하며

추가로 지난

1년간 8천명

이상의 관광객

유치한 국제여행알선업도

가능 International

Tourism

Company

recruiting

more than

8,000 tourist

for past

1 year.

|

-

- One

of the most significant

benefits in incorporating

your business is

the fact that LLC

owners are not personally

liable for the debts

and obligations

of the LLC. However,

sole proprietorships

and general partnerships,

as well as corporations,

can be held personally

liable for such

debts. Therefore,

if a shareholder

acquired $100 in

stock, he or she

is only responsible

to the company for

$100 of that stock.

-

- Other

benefits include

the following:

- •

Tax flexibility

and other tax-related

benefits. For example,

corporations are

taxed at a lower

rate than the individual

rate and own shares

in other corporations.

Only 20 percent

of the dividends

from these holdings

are taxable. Corporations

can carry an unlimited

amount of losses

into future tax

years to offset

their taxable income,

while sole proprietors

can only carry forward

$3,000 in losses.

- •

Deductibles for

business expenses

- •

Brand protection

- •

Added credibility

- •

Easier to obtain

financing if incorporated

- •

Increased customer

base as clients

want to know that

they can trust the

business. Therefore,

if the business

is incorporated,

there is an added

level of credibility,

which in turn, can

increase your client

base.

- •

Structure flexibility

- •

Unlimited growth

- •

Investment opportunities

- •

The ability to have

a separate credit

rating and build

a separate credit

history

-

- You'll

also want to determine

where you should

incorporate. States

like Delaware, California,

Nevada, Maryland,

Pennsylvania, and

Connecticut are

favorable states

in which to incorporate.

While most people

incorporate their

business in the

state they live

and conduct most

of their business,

some business owners

have found it beneficial

to incorporate in

any one of the aforementioned

states.

- Corporations

and LLCs can own

property, thereby

increasing their

assets and revenue

by holding such

an asset. But if

either type of business

incurs debt, that

property could be

affected. Now let's

assume you own a

corporation. You

have your own personal

property –

your home. If the

corporation incurs

debt, your own personal

property could in

fact be affected.

However, if you

are an LLC owner,

your personal assets

cannot be affected.

Therefore, any debts

or obligations that

arise out of the

operations of an

LLC cannot reach

the LLC owner.

-

- 세금

|

-

- 사업세는 법인소득세,

직원사회보장세,

직원의료보장세 등이

있으며 주별 사업세가

적은 순서는

델라웨어주가 가장 적고 <

오리건 < 콜로라도

< 유타 < 아이다호

< 캘리포니아 <

네바다 < 플로리다

< 텍사스 < 애리조나

< 일리노이 < 와싱턴

< 뉴멕시코 <뉴욕주가

가장 많다.

-

- 1.

법인세

-

- 1)

연방(Federal)법인세:

- 회계기준에 따라 결산한

당기순이익에 세법상

여러 조정사항들을

반영하여 산출한 과세소득 기준으로 누진세율 적용.

과세소득이 1천만 달러 이상일

경우 35%. 주마다 다르지만

대략 5~9% 정도.

- 지사가 영업을

하지 않는 경우, 한미조세협약에 따라 연방법인세의 적용을 받지

않으나 뉴욕주처럼 영업을

하지 않는 외국법인에도 매년 일정액의

수수료($300)를 받는

주도 있dma.

- 연방법인세

비적용 대상은 고정사업장(permanent

establishment)으로 간주되지

않을 경우, 상품저장,

전시 혹은 배달 목적으로

미국내 시설사용/미국내 보유

경우, 상품을 제3자를

위하여 가공하기 위한

목적으로 미국내에서

보유하는 경우, 한국회사를

위한 상품구입, 정보수집의

목적으로 고정사업장을

유지하는 경우, 한국회사를

위하여 광고, 정보 공급,

과학적 연구 혹은 이를

위한 예비적 보조적 성격을

지닌 유사한 활동을 위하여

고정 사업장을 유지하는

경우.

-

- 2) 주(State)소득세:

대부분의

주는 연방 정부의 한미조세협약을 인정하지

않고 본사의 당기 손익에

대하여 해당 주의 영업

비율에 따라 법인세를

부과.

-

-

- 2.

개인세 -

연방소득세(Federal

Income Tax)와 주소득세(State

Income Tax)

- .

- -

누진세율

적용. 연방소득세는

소득에 따라 10%~35%, 주정부소득세는

주마다 다름.

- -

신고는 연방정부와

주정부 두 곳에 매년

신고,

- - 회사

연말정산과 별개로

본인 및 배우자가 세금신고서

작성

서명하여 발송.

- -

신고양식은 국세청(www.irs.gov),

주정부 홈페이지,

우체국, 도서관에 비치.

-

- 3.

사회보장세(Social

Security Tax)

-

- 4.

의료보장세(Medicare

Tax)

-

- 5.

사업자납세번호 (E.I.N.

Employer Identification

Number)

- FORM SS-4를

작성해 미 국세청(IRS)으로

우편/팩스/전화/인터넷으로

신청. 작성: 회사명/주소/회사설립 주 및 카운티

명/EIN 신청자명

및 SSN 번호 (SSN

없는 경우 외국인

개인 납세자 번호 ITIN

(Individual Taxpayer

Identification Number

기입)/회사 형태/사업특성/신청사유/예상개업일/회계연도/최초임금지급일/향후

1년간 예상채용인원).

-

-

-

고용 Employment

|

-

-

- -

파견: 본사 파견 직원수에

대한 규제는 없으며,

업무관련 자격을 증명해야 함.

- -

채용: 현지 시민권자/영주권자를

채용해야 함.(국제법률연구원(www.ilri.co.kr)

자료 무단게재 엄금)

* 면접시

질문금지사항: 생년월일,

결혼/재혼전 이름, 결혼 여부,

배우자 이름, 배우자의

직장,

자녀의 수 및 나이, 국적, 인종,

성별, 종교, 노조활동,

급여압류여부 등. 범죄경력은

질문할 수 있으나 채용거부사유는 안됨.

- -

해고: 해고시

차별대우소송을

예방하기

위해 해고사유가 있다는

점과 모두에게 일관된

징계절차가 적용되었다는

것을

증명해줘야 함. (사실조사,

해고결정에 대한 변론,

단계적 징계 등

인사관리규정과 일치,

증인, 해고통보할 때 ‘결정되었다,

문제가

있다'는 표현

금지, 해고결정근거 설명하고,

실업수당과 고용추천

상담내용과

결과 기록, 물리적 행동(폭력)

할 가능성에 주의하여

대처.

- -

감원(Downsizing the

Workforce) : 사전에

감원 대상자 선정을 위한

정당한 기준수립. * 일관성

있는 기준을

적용. 부적절한 감원

계획은 소송으로 인한

비용상승, 각종 차별

소송에 의한배상금, 잔류한

직원의 근로의욕

저하의 위험이 있음.

-

|

|

.gif)